FOMC Post-Mortem: Warsh is Hawkish

Fed Jun Meeting 17.06.2026

This one’s on us.

The complete archive, podcast and video are one step away!

25% off the annual plan, code “SUB25LBM”, 8 days only.

Overview and Policy

As usual, we try to make a long story short: Wash is hawkish, the FOMC is hawkish, the Economic Projections are hawkish. Price stability is the main, if not the sole concern of the Committee at this stage: vindicating our long-standing view on all of the above.

The way Warsh has been talking up his resolve to enforce price stability, at 2.0% inflation, after years of overshooting is surely a change. His implicit acknowledgement that unemployment is not the main concern, is surely correct, and in line with our thoughts.

We found two comments by Warsh worth reporting, apparently trivial, but not necessarily so at the Fed, in view of their dual mandate:

There is no trade-off between unemployment and inflation; and

The Fed's job is to prevent second-round effects.

Although Warsh is refraining from forward guidance, the indications stemming from the Macroeconomic Projections (SEP) are clear (see Section 2):

The Inflation projections have been revised upward, meaningfully, showing a larger, and persistent overshooting of the 2% - reiterated - target.

The Rate projections (Dots), consistently, have been also revised upward aggressively, and are now consistent with a rate hike in the pipeline.

The indications could not be clearer: the Committee thinks that policy has to be tightened.

Hence, the knee-jerk market reaction was to converge - further - towards our rate view (+50bps by year-end), pricing in a full hike by Oct and 2 by Apr.

Here are some catches however, that we will be monitoring in the coming months, all having to do with the working groups announced by Warsh:

The Fed's Balance Sheet

Warsh has announced a working group dealing with the Fed's Balance Sheet.

Surely, as said, the FOMC inflation projections require some policy tightening.

The market has interpreted, understandably, this tightening as rate hikes, our long-standing view, and the yield curve has flattened aggressively.

However, we reckon that, eventually, as per Warsh's long-standing conviction, the tightening may occur via a Fed's balance sheet reduction.

Probably there will be no time should the tightening occur sooner rather than later, but it is a risk still worth monitoring.The Data

Warsh has announced also a working group on economic data.

The Chairman was very adamant in enforcing the notion that the Fed inflation target is at 2.0%.

We want to hope that the working group does not redefine inflation so that, by magic, we are at target rather than above.

In our view, inflation is far more pernicious in the US than it is in Europe.

Indeed, in Europe, from the EMU to the UK, high inflation is at the moment, by and large, due to supply conditions.

In the US, instead, it is due to both supply and demand, thus challenging even more central banks and requiring more, and long-lasting tightening.

Last, but not least, two comments by Trump look like a game-changer:

"Alright they kept rates stable, whatever".

On the Fed possibly raising rates: "it could happen".

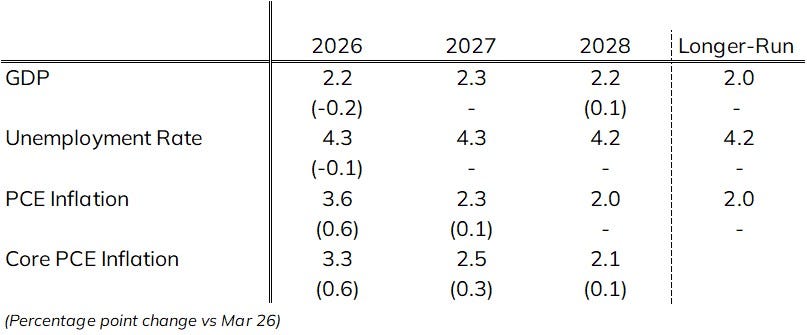

Jun Summary of Economic Projections (SEP)

The Fed's SEP unambiguously sent a hawkish message, primarily through its inflation f/c and the upward shift in the distribution of its policy f/c dots.

Indeed, despite moderately revising growth lower for the year, the FOMC median projection still envisaged:

PCE inflation:

Much higher at 3.6% this year, up 0.9pp, with the central tendency around this f/c narrowing from 0.5pp to 0.2pp.

Slightly higher in 2027, up 0.1pp to 2.3%, thus extending the duration of above target inflation.

Core PCE inflation:

Revised up 0.6pp to 3.3% this year, reflecting a broader inflation shock than expressed solely by the direct effects from higher energy prices.

Revised up 0.3pp to 2.5% in 2027 and 0.1pp to 2.1% in 2028, reflecting a more durable source of inflation.

Unemployment:

A slightly lower Unemployment rate of 4.3% in 2026, close to its estimate of full employment (4.2%).

Table 1: FOMC Macroeconomic Projections

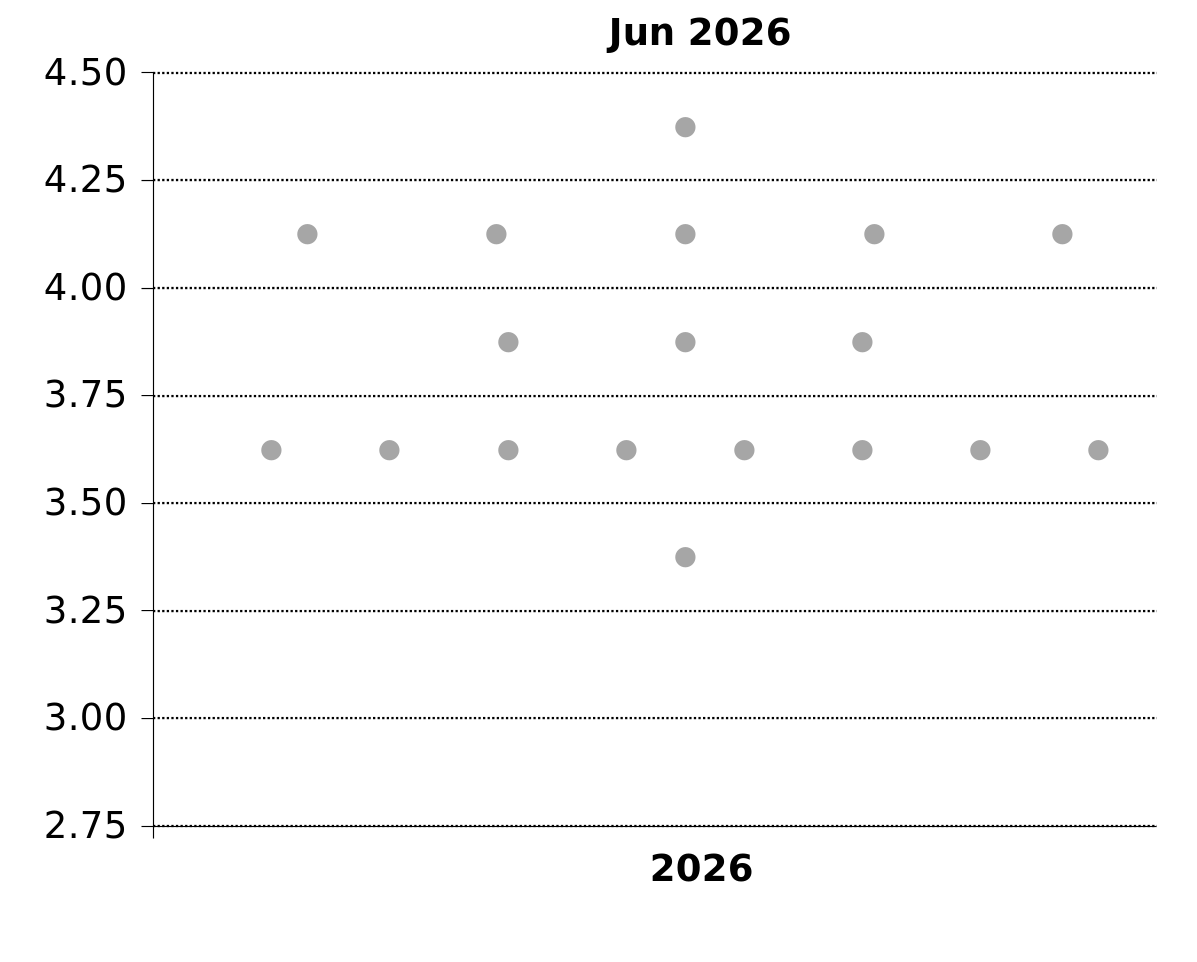

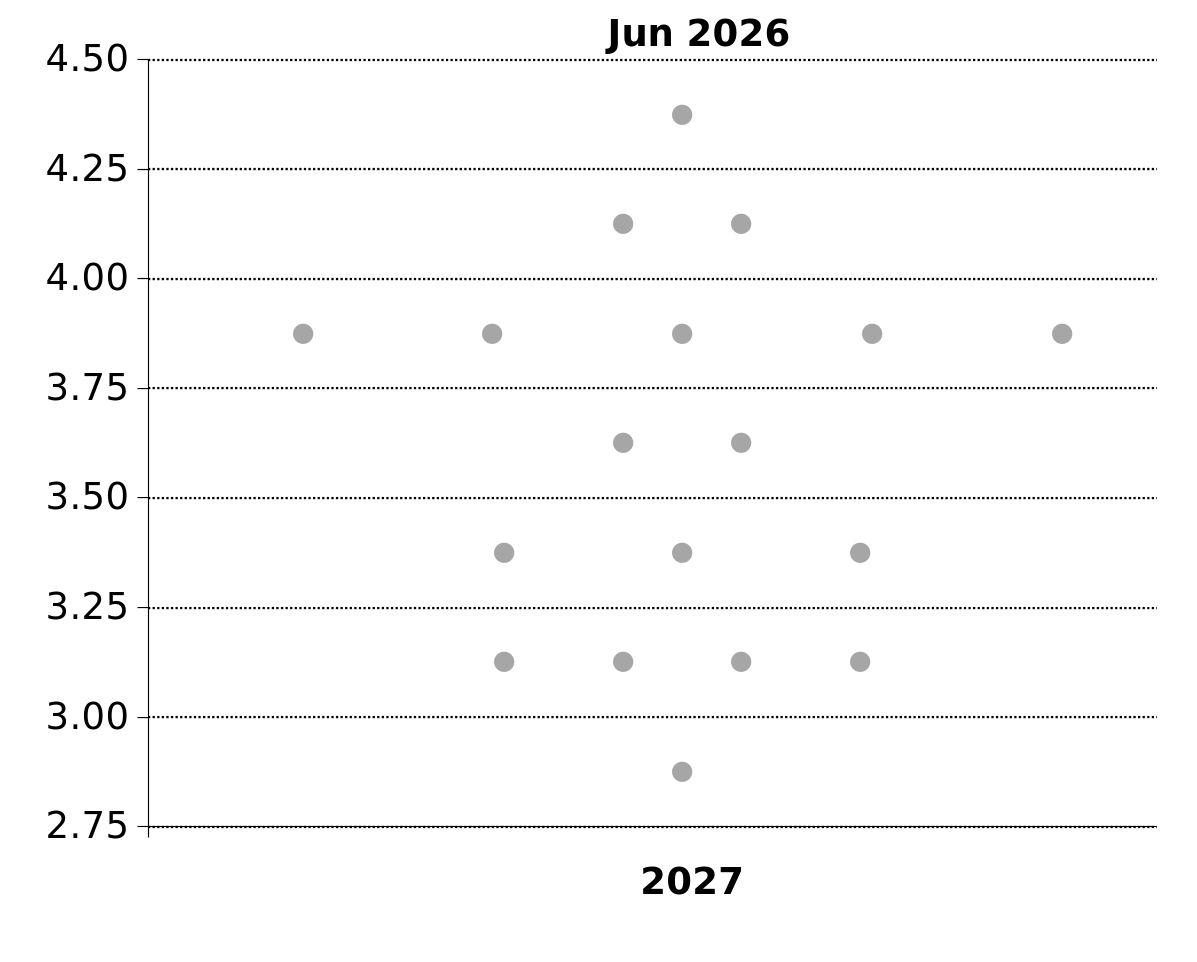

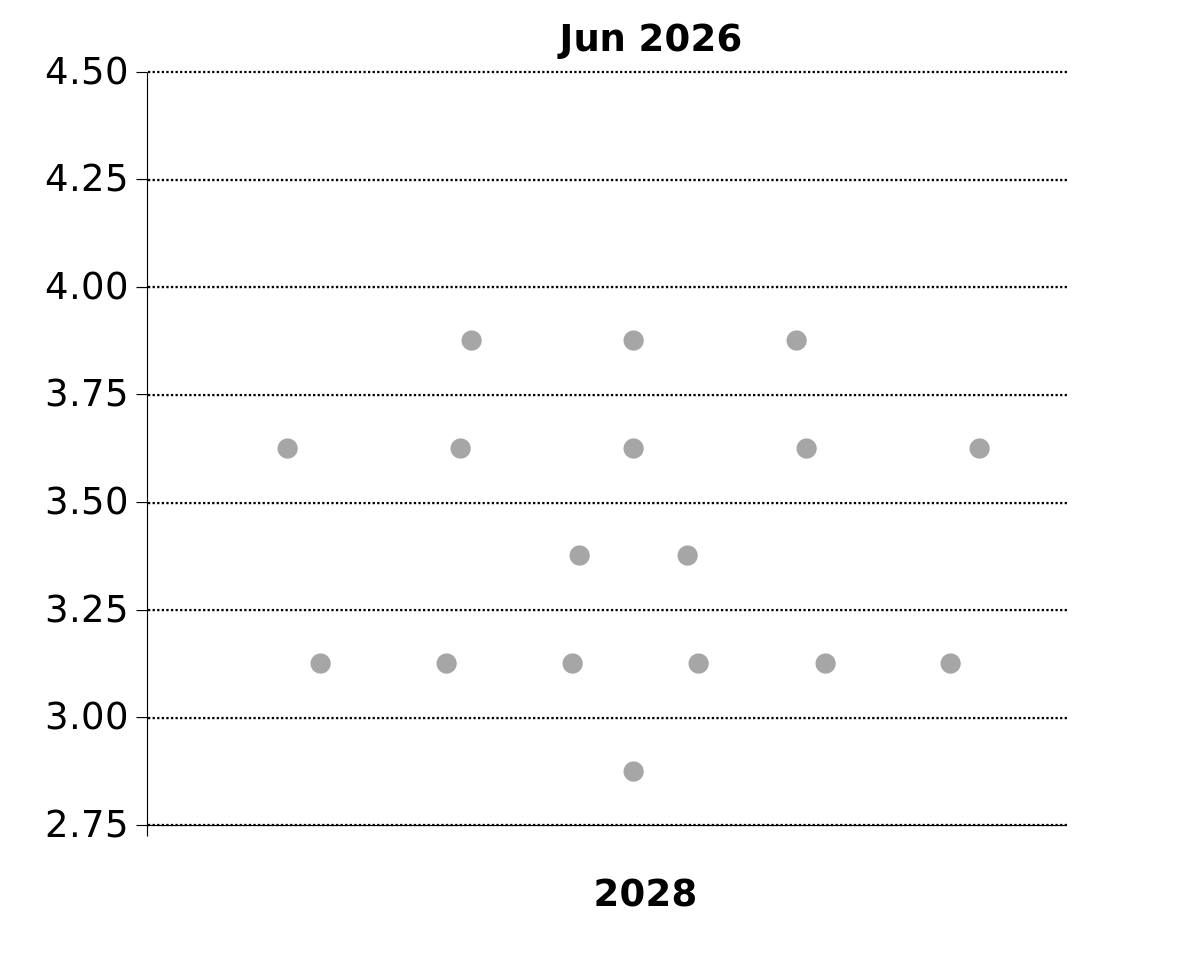

As mentioned, the FOMC also delivered its hawkish message through its policy projection "dots".

Here, the main message stems more from the mean as opposed to the median, reflecting a more hawkish skew.

Although both median and mean shifted higher relative to Mar throughout the f/c horizon, except for the long-run where the median fell marginally.

Indeed, the Dots, which omit Chair Warsh's f/c throughout and Governor Powell's dot beyond 2027, shifted to show:

In 2026:

A median f/c of 3.75%, up 38bps from Mar and thus unwinding expectations of a cut in favour of a hike with a 50% probability.

A mean f/c of 3.83%, up 48bps from Mar, thus envisaging a rate hike this year.In 2027:

A median f/c of 3.625%, up 50bps from Mar, unwinding expectations of two cuts previously in favour of just half a rate cut back to current levels.

A mean f/c of 3.60%, up 41bps from Mar, suggesting less upside risk than previously, partly due to tighter policy.In 2028:

A median dot of 3.38%, up 25bps from Mar to maintain the view of one cut that year.

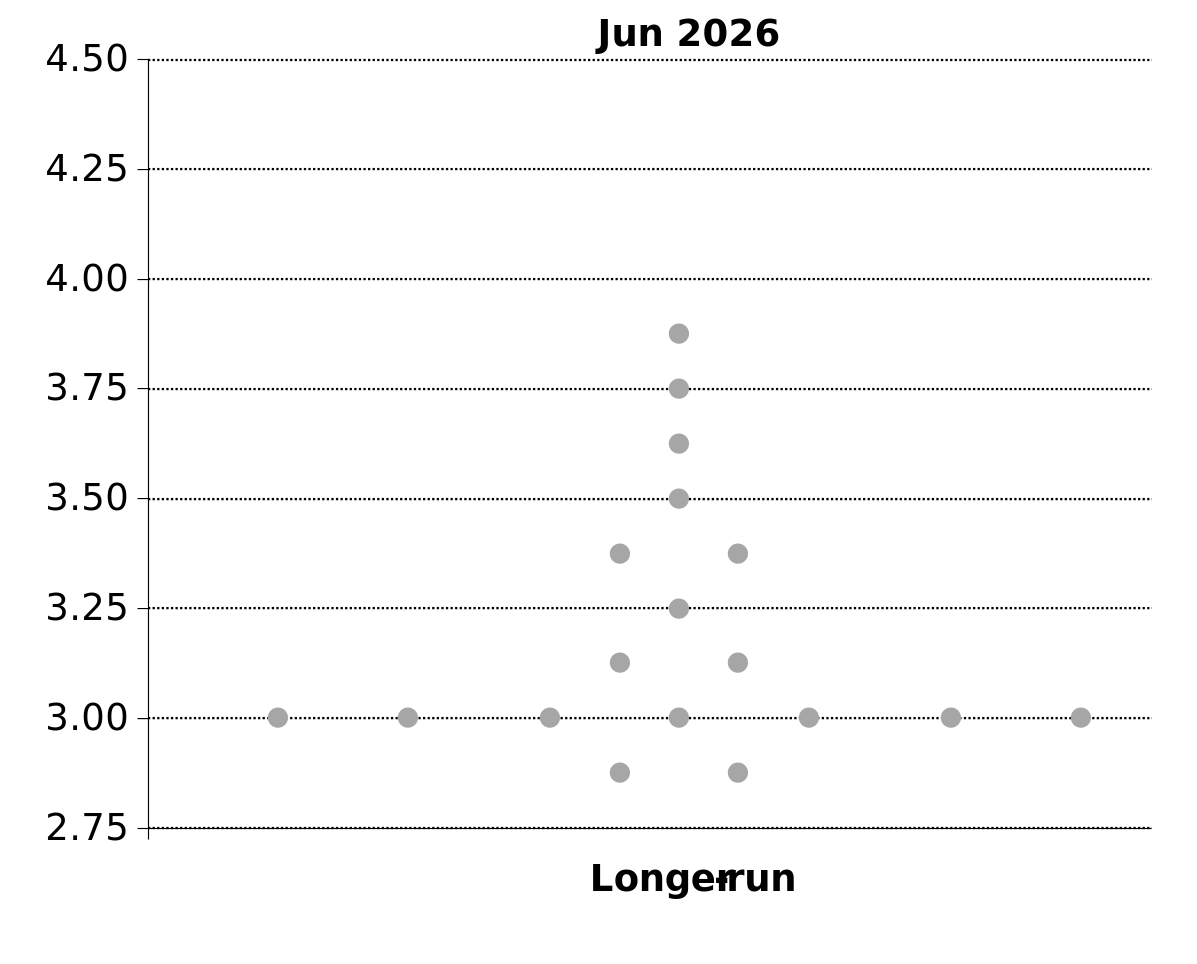

A mean dot of 3.42%, up 23bps, again to show a slight hawkish skew.In the Longer Run:

A median f/c of 3.06, down 6bps from Mar.

A mean f/c of 3.21%, up 4bps from Mar.

We would also highlight that as well as a more hawkish distribution and skew, the range of f/c has also narrowed. Indeed, the overall range has narrowed 25bps to 1pp in 2028 and the Longer-Run, although we suspect this is due to the exit of uber-dove Miran.

Fig. 1: Dots Skew in Favour of Hike This Year...

Fig. 2: ... Reversal to Current Level in 2027...

Fig. 3: .... One Cut in 2028...

Fig. 4: ... An Upwards Reassessments of Neutral

Enjoyed this read? It’s just a taste of what we publish.

Our first-ever discount is still on: 25% off the annual plan.

Use code SUB25LBM — it expires June 26th, just 8 days left!

Authors

Disclaimer: LB MACRO commentary and forecasts are solely for information purposes; it is not investment research or advice and should not be regarded as an offer or solicitation to buy any instruments mentioned – it should be regarded as unregulated by the Financial Conduct Authority. LB MACRO does not accept liability for the use of, or reliance on, this document and/or its contents by any other party. No personal recommendation is being made to you – any strategies referred to may not be suitable for you and should not be relied upon as a substitute for your independent judgement. Past performance or future forecasts are not a reliable indication of future expectations and investors should be aware that losses and costs can occur on any investment. LB MACRO cannot accept liability for direct or indirect damages, or loss of returns in any way from information provided. Every effort has been made as to the accuracy and information from sources believed to be reliable, but the contents of this document have been made without any substantive study being undertaken into the sources. LB MACRO does not take responsibility for the accuracy or completeness of information provided in this document. By accepting this document you agree that you have read the above disclaimer and to be bound by it.